India plans to use crypto tokens in upcoming native web browser

The feature is envisaged as part of the country’s national web browser project.

Čítaj viac

The feature is envisaged as part of the country’s national web browser project.

Čítaj viac

The lower house in the parliament of India approved updates to a bill that would ease data storage, processing and transfer standards for BigTech companies.

Čítaj viac

In an RBI-organized conference for the directors of Indian banks, deputy governor Mahesh Kumar Jain discussed risk strategies around sustainable growth and stability.

Čítaj viac

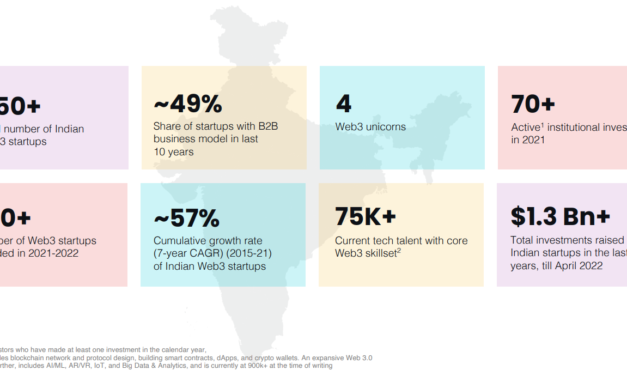

The global Web3 boom is expected to add $1.1 trillion to the Indian economy over the next decade, supporting the investment-based momentum driven by over 450 in-house startups, including CoinDCX, Polygon and CoinSwitch. A recent study from the National Association of Software and Service Companies (NASSCOM), an Indian non-governmental trade association and advocacy group, highlighted India’s position as a leading global player in the Web3 market owing to several factors spanning a large talent pool, high adoption rate and product development for international markets.Snapshot of India’s Web3 startup ecosystem in 2022. Source: NASSCOMThe US-India Strategic Partnership Forum (USISPF) estimated that “Web3 can add $1.1 trillion of new economic value to the Indian GDP in the next 10 years.” Investments in Indian Web3 startups. Source: USISPF and NASSCOMMoreover, the study highlighted that investments in Indian Web3 startups mimicked crypto adoption by racking up a 37x growth over the last two years. The explosive Web3 growth in the country is further supported by an increasing talent pool, which makes India’s demand-supply gap the lowest when compared to the USA, China and UK.In addition, India ranks first when it comes to reskilling in newer technologies, which is considered paramount in emerging technologies such as Web3 and blockchain. Global Web3 talent distribution. Source: OKX and NASSCOMThe above graphic shows the global talent pool for Web3, showcasing the US and China overpowering India. However, the study estimates that India’s Web3 talent pool is expected to experience the fastest growth rate in the coming 1-2 years.Focus areas for Indian Web3 startups. Source: Zinnov CoNXT Research & AnalysisThe Indian Web3 ecosystem caters to a variety of real-world applications and roughly 60% of the local startups expanded their footprint outside India.Related: India aims to develop crypto SOPs during G20 presidency — Finance ministerIndian e-commerce giant Flipkart recently launched a metaverse space — named Flipverse — for locals to try out and purchase merchandise from brands including Puma and Nivea. Flipverse was developed in collaboration with Polygon-incubated organization eDAO and will support digital collectibles and be made available on Flipkart’s newly online shopping platform, FireDrops.

Čítaj viac

The Enforcement Directorate of India (ED) unfroze the bank accounts of the Indian crypto exchange WazirX, according to a statement from the exchange released on Sept. 12.WazirX says it has been cooperating with local authorities during their anti-money laundering (AML) investigation by providing all of the necessary documents and details requested. The investigation targeted 16 fintech companies and instant loan apps, some of which solicited services from the exchange.The exchange, however, said it has a no-tolerance stance towards any illegal activities on the platform. Additionally, it said that most of the targeted users in the ED investigation had already been flagged as suspicious by WazirX and blocked in 2020-2021.WazirX told Cointelegraph the case is still under investigation but funds have been unfrozen due to no suspicious activity found, with “no further comment as of now.”Funds in WazirX bank accounts had been frozen since Aug. 5, when the ED initially announced the investigation. The locked funds amounted to over $8.1 million in total.ED searches the Director of WazirX Crypto-Currency Exchange & freezes its Bank assets worth Rs 64.67 Crore for assisting accused Instant Loan APP Companies in laundering of fraud money via purchase & transfer of virtual crypto assets.— ED (@dir_ed) August 5, 2022The ED’s accusations against WazirX claimed it had processed $130 million in transfers of funds to wallets under investigation for illegal activities. In light of the accusations, Binance, which once tried to acquire the company in 2019, distanced itself from the exchange via a public statement from CZ on Twitter.Related: Binance sides with Indian regulators in WazirX fallout to cease support for off-chain transfersPrior to the recent activity, the exchange was under ED investigation in 2021 for money laundering charges related to illegal online gambling proceeds tied to Chinese entities.This time around, the crackdown on crypto exchanges in the country did not stop with WazirX. On Aug. 12, the ED froze a total of $46.4 million in Yellow Tune’s bank balances and balances from crypto exchange Flipvolt. The allegations were also money laundering related, and the company was accused of being a shell for Chinese entities.Authorities said the funds would remain unavailable until the exchange can account for the criminal proceeds that it transferred out of the country.These investigations began to pile up after the Indian government announced crushing new crypto tax regulations, which came into effect earlier this year.

Čítaj viac

India’s Directorate of Enforcement, or ED, has announced it froze roughly $8.1 million in funds and conducted a search connected to cryptocurrency exchange WazirX as part of an investigation into instant personal loan fraud.In a Friday announcement, the Directorate of Enforcement alleged WazirX facilitated transactions by unnamed fintech firms “to purchase crypto assets and then launder them abroad” as part of a scheme involving Chinese-backed companies circumventing India’s licensing regulations. In its investigation, the ED said it ordered WazirX bank accounts containing 646.7 million Indian rupees — roughly $8.1 million at the time of publication — frozen and conducted a search connected to co-founder Sameer Mhatre.According to the regulator, the investigation was still ongoing. However, the ED claimed the crypto exchange had “lax KYC norms” and “loose regulatory control” of transactions between WazirX and Binance, and did not record the information needed to verify the origin of the funds used to purchase crypto in the alleged fraud. “Despite giving repeated opportunities, WazirX failed to give the crypto transactions of the suspect fintech APP companies and reveal the KYC of the wallets,” said the ED, adding:“WazirX is not able to give any account for the missing crypto assets. It has made no efforts to trace these crypto assets. By encouraging obscurity and having lax AML norms, it has actively assisted around 16 accused fintech companies in laundering the proceeds of crime using the crypto route.”ED searches the Director of WazirX Crypto-Currency Exchange & freezes its Bank assets worth Rs 64.67 Crore for assisting accused Instant Loan APP Companies in laundering of fraud money via purchase & transfer of virtual crypto assets.— ED (@dir_ed) August 5, 2022In a Friday Twitter thread, Binance CEO Changpeng Zhao said the firm did “not own any equity in Zanmai Labs, the entity operating WazirX and established by the original founders.” He added that “Binance only provides wallet services for WazirX as a tech solution,” while WazirX was responsible for KYC and other operations on the exchange. Related: Indian regulator probes crypto exchange for alleged forex law violationsWith the exodus of many crypto firms in China following a regulatory crackdown, many companies have reportedly turned to the markets in India. The ED reported that some fintech firms “backed by Chinese funds” had “piggybacked” on Indian companies with defunct non-banking financial company licenses to offer lending services to residents.The ED took similar action against WazirX in June 2021, ordering the crypto exchange to show cause related to transactions of a money-laundering investigation into illegal online betting applications involving Chinese nationals. WazirX director Nischal Shetty said at the time that the exchange went “beyond [its] legal obligations by following Know Your Customer (KYC) and Anti Money Laundering (AML) processes and have always provided information to law enforcement authorities whenever required.”Cointelegraph reached out to WazirX, but did not receive a response at the time of publication.

Čítaj viac

Indian finance minister Nirmala Sitharaman has called for global collaboration on cryptocurrencies, assessing their pros and cons to form a common standard and taxonomy.Addressing a question on cryptocurrency in the Lok Sabha, the lower house of the Indian parliament, Sitharaman said that the Indian central bank had advised the government to prohibit the use of cryptocurrencies as it poses a risk to financial stability. However, the government is looking for a global approach. She said:”Any legislation for regulation or banning can be effective only after significant international collaboration on evaluation of the risks and benefits and evolution of common taxonomy and standards.”She also reiterated the Indian central bank’s stance on crypto’s value is based on speculation. She added that “the value of fiat currencies is anchored by monetary policy and their status as legal tender. However, the value of cryptocurrencies rests solely on the speculations and expectations of high returns that are not well anchored.”Reserve Bank of India (RBI), the Indian central bank, has maintained an anti-crypto stance since 2013, issuing multiple advisories against investing in digital assets and even prohibiting banks from offering services to crypto firms in 2018. The banking ban was eventually overturned after a supreme court ruling in 2020.While the Indian government is yet to decide whether to move ahead with a ban or regulate the nascent crypto sector, the government was relatively quick to propose and implement two crypto tax laws that have wreaked havoc on the budding crypto industry.Related: The regulatory implications of India’s crypto transactions taxDuring the January parliamentary session, the finance minister announced a 30% tax on unrealized gains and a 1% tax deduction at the source (TDS). The laws were heavily inspired by the country’s gambling and betting laws, resulting in an instant decline in trading volume across exchanges just weeks after the new 30% tax came into effect.The trading volumes and trader interests plunged further after 1% TDS came into effect on July 1. Many thriving crypto unicorns hopeful of a positive regulatory approach have started shifting their bases to crypto-friendly legislation, such as Dubai and Singapore.

Čítaj viac

The Indian crypto landscape lost some momentum this year as the government introduced two laws demanding crippling taxes on crypto-related unrealized gains and transactions.India’s first crypto law, which requires its citizens to pay a 30% tax on unrealized crypto gains, came into effect on April 1. A commotion among the Indian crypto community followed as investors and entrepreneurs tried to decipher the impact of the vague announcement with little or no success.Knowing that India’s second crypto law — a 1% tax deduction at source (TDS) on every transaction — would translate into an even greater impact on trading activities, numerous crypto entrepreneurs from India considered moving bases to friendlier jurisdictions. Following the imposition of additional taxes, Indian crypto exchanges reported a massive drop in trading volumes. Data from CoinGecko confirmed that trading volumes on Indian crypto exchanges are down 56.8% on average as investors eye off-shore exchanges to cut their losses on unforgiving taxes. However, India’s finance minister Nirmala Sitharaman previously acknowledged the resultant backlash and revealed plans to reconsider amendments to crypto-related taxes upon careful consideration. Grassroot impact of crypto regulations in IndiaWithin just days of implementing India’s infamous crypto laws, crypto exchanges in the region reported a massive slump in trading volumes. Nihal Armaan, a small-time crypto investor from India, told Cointelegraph that taxation is not a deterrent when dealing with cryptocurrencies. Instead, he compared the imposition of a flat 1% tax as a way of capital lock-in, a feature used by corporates to prevent investors from taking away their funds, adding that “The TDS isn’t the issue, the amount of TDS is — since it evidently reduces the number of trades a person can carry out with their capital at hand.”The North Block of the Central Secretariat, the residence of the Chairperson of the Central Board of Direct Taxes, New Delhi. Source: Edmund Gall.Kashif Raza, founder of crypto education startup Bitinning, told Cointelegraph that implementing TDS is a good first step in ring-fencing the crypto industry in India. While Raza added that investors like himself who trade less might not feel the repercussions of such a law, he did acknowledge that “the amount of TDS is a topic of debate as there are many active traders in the crypto industry who have been affected by this decision.”Contrary to the popular belief of trade slowdowns, Om Malviya, president of Tezos India, told Cointelegraph that he envisions little to low disruption for long-term investors. Instead, he expects pro-crypto reforms in the current laws over the next three to five years. While awaiting friendlier tax reforms, he advised investors to gain a deeper understanding of the technology, adding, “Even the users from smaller cities will be forced to study the cryptocurrency, study about the team and technology and the fundamentals behind it, and then make any investment or trading decision.”Rajagopal Menon, vice president of crypto exchange WazirX, told Cointelegraph that despite falling trading volumes, the exchange continues to focus on complying with the new taxes rules and meeting the standards set by the local regulators, adding, “The TDS will not affect the serious crypto investors, a.k.a, hodlers, as they have a long-term horizon in mind.” In 2021, the exchange witnessed over 700% growth in signups from smaller cities such as Guwahati, Karnal and Bareilly.Recent: Crypto payments gain ground thanks to centralized payment processorsHowever, Anshul Dhir, chief operations officer and co-founder of EasyFi Network — a layer-2 decentralized finance (DeFi) lending protocol — told Cointelegraph that unless the Indian government introduces friendlier crypto regulations with prolonged exposure to taxes, passionate investors may join crypto entrepreneurs in the exodus away from India.Crypto taxes and the creation of long-term holders While the crypto trading volume has seen a drastic reduction across Indian exchanges, it indicates investors’ willingness to hold on to their assets until pro-crypto regulations kick in. In order to ensure profitable trades, Indian investors speaking to Cointelegraph revealed that they have been waiting for a bull market to sell a part of their holdings for profits. Concurring with this change in the present investor mindset, Malviya added that “if you want to pay this amount of high taxes, you have to be really sure that your investment is going to be worth more than what you’re more than today.” Armaan reiterated that the TDS itself is not a deterrent to crypto traders, but “the 30% tax on profits without the provision to set off losses is harsh and discourages any new trader even to try trading in the cryptocurrency industry.” Even though many Indians welcomed the tax regime, as it gives a sense of legitimacy to the crypto industry in the country, Dhir believes that “the tax rate is a deal-breaker and will cause a lot of prospective investors to hold their investments in virtual digital assets.”On this front, Menon warned investors against trying to find loopholes in the law by using foreign exchanges, peer-to-peer sites and decentralized exchanges. Regardless of the platforms used, all Indian citizens are liable to pay the TDS; failure to do so would result in non-compliance with the existing tax laws of the land. The slowdown in trade volumes was accompanied by a drop in liquidity, which also impacted the global liquidity for the overall crypto ecosystem. India’s interaction with CBDCsCentral banks worldwide seem to have unanimously agreed on either experimenting with or launching their own versions of central bank digital currencies (CBDC). India, on that front, is expected to introduce a digital rupee by 2022–23. According to the country’s finance minister, Nirmala Sitharaman, it is expected to provide a “big boost” to the digital economy.While CBDCs fundamentally differ from how cryptocurrencies operate, governments are in a race to create a fiat-based system that incorporates the best features offered by the crypto ecosystem. Raza added that a CBDC backed by the Indian rupee “will help in faster and cheaper inward remittances and global payments” but doubts its acceptance as a store of value by retail.As pointed out by Malviya, CBDCs are well suited to cater use cases that demand immediate issuance of funds, adding, “but it is not going to void the case for cryptocurrencies essentially.” Dhir, however, believes that CBDCs will complement the digital asset industry, particularly the DeFi projects. Moreover, India’s central bank, the Reserve Bank of India, needs to formulate policies conducive to innovation and growth and highlight the positives of the budding technology to the general public.For many, India’s crypto taxes seem like a proactive move to discourage trading. Still, speaking from an investor’s point of view, Armaan argued that the government did the best they could in terms of explaining the tax structure with the information they had at their disposal. The waiting gameFriendlier tax reforms are a waiting game for Indian entrepreneurs and inventors, but both communities have to be compliant while preparing for greener pastures. For investors, this means educating themselves about the ecosystem and best practices for trading. Armaan’s approach in the current scenario is to have low allocation and a systematic investment plan approach to investing. In addition to being watchful of the market developments, Dhir advises the community to engage with the government in their own capacities with a positive frame of mind and not engage in antagonistic banter on social media. “The new use cases, new projects and new products are only going to come out and this space is only going to get bigger. So if you do want to part or not, you have to do your own research, and you have to be committed,” added Malviya.Recent: Andorra green lights Bitcoin and blockchain with Digital Assets ActMenon recommended that entrepreneurs keep engaging with the government in the hopes that it will tweak its policies one day. “Parallelly, all the developments need to be shared with the government as well, so they are aware of the innovation happening in this space by the talent at home; this may have an overall positive impact on the industry at large,” added Raza.Furthermore, Malviya stated that entrepreneurs must be committed to the cause as they strive to build solutions catering to a growing number of use cases, adding that “you don’t necessarily have to focus on shifting out of India; I think the first focus should be what problem you’re trying to solve.”In the meantime, investors are hopeful for constructive frameworks around cryptocurrencies to help weed out bad actors from the equation.

Čítaj viac

In discussion with the International Monetary Fund (IMF), T Rabi Sankar, the deputy governor of the Reserve Bank of India (RBI), reflected an anti-crypto stance as he spoke about India’s potential to disrupt the crypto and blockchain ecosystem. Rabi Sankar started the conversation by highlighting the success of the Unified Payments Interface (UPI), India’s in-house fiat-based peer-to-peer payments system — which has seen an average adoption and transaction growth of 160% per anum over the last five years. “One of the reasons it is so successful is because it’s simple,” he added while comparing UPI’s growth with blockchain technology. According to Rabi Sankar:“Blockchain, which was introduced six-eight years before UPI started, even today is being referred to as a potentially revolutionary technology. [Blockchain] use cases haven’t really been established that much at the speed it initially was hoped for.”However, the RBI official confirmed that a large population in India still lacks access to UPI-based banking due to the unavailability of smartphones. To counter this, the Indian government is working on offline payment platforms, some of which have started rolling out to the masses.June 2 at 7:00am ET // At the Frontier: India’s Digital Payment System and Beyond will explore the latest developments in digital payments with a focus on lessons from India as well as future with a significant role for Central Bank Digital Currencies. https://t.co/ZSj7i15fBG pic.twitter.com/X6cVyHewEs— IMF (@IMFNews) May 31, 2022Rabi Sankar also stated that banks will remain crucial for providing liquidity services to the general public in India, warning that technology is merely a tool and cannot be used to create currencies:“A currency needs an issuer or it needs intrinsic value. Many cryptocurrencies which are neither are still being accepted at face value. Not just by gullible investors but also the experts, policymakers or academicians.”He further stated that RBI does not believe that stablecoins, like Tether (USDT), should be accepted blindly as 1-to-1 fiat pegged currencies. Speaking about the advantages of a digital rupee, Rabi Sankar said:“We believe that central bank digital currencies (CBDCs) could actually be able to kill whatever little case that could be for private cryptocurrencies.”Related: India to roll out CBDC using a graded approach: RBI Annual ReportOn May 28, India’s central bank, RBI, proposed a three-step graded approach for rolling out CBDC “with little or no disruption” to the traditional financial system.As Cointelegraph reported, finance minister Nirmala Sitharaman first revealed the plan to launch a CBDC in 2022-23 with an aim to provide a “big boost” to the digital economy. RBI’s report revealed that the central bank is currently experimenting to develop a CBDC that addresses a wide range of issues within the traditional system.

Čítaj viac

The Department of Economic Affairs of India is finalizing a consultation paper on crypto currencies, which then will be handed over to the federal government. The implementation of the document could bring the country of 14 billion people closer to the international regulatory consensus on digital assets. On Monday, May 30, during an event hosted by the Ministry of Labour and Employment, Economic Affairs Secretary Ajay Seth revealed that his department is finishing the work on the consultation paper, which would define the nation’s stance on crypto. The document was crafted in cooperation with industry stakeholders, the International Monetary Fund (IMF) and the World Bank. Seth specified that the paper would strengthen India’s commitment to “some sort of global regulations”:“Digital assets, whatever way we want to deal with those assets, there has to be a broad framework on which all economies have to be together.”Answering the question about the possible outright ban, the official acknowledged that any national-level prohibition wouldn’t work in isolation: “Whatever we do, even if we go to the extreme form, the countries that have chosen to prohibit, they can’t succeed unless there is a global consensus.”Related: Indian government’s ‘blockchain not crypto’ stance highlights lack of understandingIn recent years India has been demonstrating a rather militant posture when it comes to crypto. In 2017 the Reserve Bank of India (RBI) and the Ministry of Finance compared the digital currencies to Ponzi schemes and prohibited any operations with them for commercial banks and lenders. In 2022, long after the ban had been formally lifted, the RBI warned about the threat of “dollarization” that crypto poses, while in his recent virtual speech at the World Economic Forum in Davos, the prime minister Narendra Modi called cryptocurrency a global challenge that demands a “collective and synchronized action” from all of the national and international bodies.

Čítaj viac

Further cementing India’s decision to introduce an in-house central bank digital currency (CBDC) in 2022-23, the Reserve Bank of India (RBI) proposed a three-step graded approach for rolling out CBDC “with little or no disruption” to the traditional financial system.In February, while discussing the budget for 2022, Indian finance minister Nirmala Sitharaman spoke about the launch of a digital rupee to provide a “big boost” to the digital economy. In the annual report released Friday by India’s central bank, RBI revealed exploring the pros and cons of introducing a CBDC.In the report, RBI stressed the need for India’s CBDC to conform to India’s objectives related to “monetary policy, financial stability and efficient operations of currency and payment systems.”Based on this need, RBI is currently examining the various design elements of a CBDC that can co-exist within the existing fiat system without causing disruptions. The Indian Finance Bill 2022, which enforced the introduction of a 30% crypto tax on unrealized gains, also provides a legal framework for the launch of a digital rupee:“The Reserve Bank proposes to adopt a graded approach to introduction of CBDC, going step by step through stages of Proof of Concept, pilots and the launch.”Halfway through 2022, at the proof of concept stage, RBI is in the process of verifying the feasibility and functionality of launching a CBDC.Related: RBI warns of crypto ‘dollarization’ of Indian economyEarlier this month, on May 17, RBI officials reportedly warned against crypto adoption citing the risks of “dollarization” of the Indian economy.As Cointelegraph reported based on the Economic Times’ findings, key RBI officials including governor Shaktikanta Das raised concerns regarding the U.S. dollar-dominated world of cryptocurrencies. An unnamed official stated:“Almost all cryptocurrencies are dollar-denominated and issued by foreign private entities, it may eventually lead to dollarization of a part of our economy which will be against the country’s sovereign interest.”“It [crypto] will seriously undermine the RBI’s capacity to determine monetary policy and regulate the monetary system of the country,” they added.

Čítaj viac

Indian crypto businesses are struggling with the new tax policies as trading volumes have dried up and many established crypto firms are looking to relocate to more crypto-friendly jurisdictions.While many developed countries and even several of its Asian counterparts are actively studying and formulating better crypto regulations, the Indian government has maintained a “blockchain, not crypto” stance. It might seem like the government is taking a cautionary step to focus on the underlying technology while keeping its distance from the volatile and risky crypto market. However, going by the recent policies and statements from the finance minister as well as sitting parliamentarians, the issue seems to be more of a lack of understanding.The newly introduced crypto tax laws, for example, are highly motivated by the country’s gambling laws and were introduced and passed hurriedly without any input from the stakeholders in the ecosystem. As many crypto pundits have warned, the harsh tax policy has driven traders away from Indian exchanges. Many ministers in the ruling government have propagated false narratives against crypto without offering any evidence to back their claims. Sushil Kumar Modi, a member of parliament from the ruling party, has compared crypto to “pure gambling” and called to “impose more tax on it so that the government can get revenue and people can be discouraged from investing in this volatile asset.” The statement is a clear example not only of a lack of understanding but of a contradiction, in that he is talking about discouraging people from investing in crypto while believing it would bring more revenue to the government.Sathvik Vishwanath, co-founder and CEO of Indian crypto exchange Unocoin, told Cointelegraph:“The government continues to see crypto as a betting and gambling alternative due to which they are only ready to support its technology but not tokens on top of it.”It is important to understand the fact that crypto and blockchain are somewhat inseparable. Crypto tokens play a pivotal role in the functioning of blockchain projects and blockchain-based rewards.Shivam Thakral, CEO of BuyUcoin, explained that a fundamental lack of understanding is one of the key reasons for such flawed policies and advocated for dialogues with specialized groups. He told Cointelegraph:“Any attempt to create an isolated policy by any country will defeat the whole purpose of blockchain technology, which is aimed at liberating the financial systems of the world. The Indian government must create specialized groups to discuss and debate finding a more accurate way to regulate the booming crypto sector in India. The time is right for India to take the lead and become the blockchain capital of the world.”While many blame the government’s lack of understanding of the nascent tech to be the key reason behind its “blockchain, not crypto” stance, others feel that India’s fintech and payments network are mature enough and that a crypto layer wouldn’t really add much utility. Thus, the government is more focused on the core technology.Trevor Goott, director of Africa and India at Unlimint — a digital financial interface provider — told Cointelegraph:“The Indian fintech and payments sector is mature and well-serviced, and crypto would just be another layer on top, so the net benefit to India would be less when compared to another country that has a less developed payment sector. Crypto will have its place in India in the medium-term, but the short-term benefits of the other blockchain products must be realized first if a choice has to be made between crypto or blockchain.”Recent: ‘DeFi in Europe has no lobby,’ says co-founder of Unstoppable FinanceIndian government sees crypto as a threatThe Indian government clearly sees crypto as a threat to its current financial system. The Indian central bank has recently warned against crypto adoption and said it could lead to the dollarization of the economy.The Reserve Bank of India said, “Crypto will seriously undermine the RBI’s capacity to determine monetary policy and regulate the monetary system of the country.”In the early days of crypto, most countries thought digital assets posed an inherent risk to their fiat ecosystem; however, as the industry matured, it has been proven that cryptocurrencies can co-exist with traditional financial markets.Siddhartha, founder of Intain — a blockchain solution firm — told Cointelegraph:“Having spoken with several people in government, they understand blockchain but are reacting in the short term to a surge of marketing dollars and campaigns that have caused a lot of noise on behalf of some crypto exchanges. These campaigns are worrisome due to the broad exposure they create among the general public. It is our view that government officials are generally supportive of blockchain that works in a manner that brings trust and transparency to the financing of non-bank financial companies.”By approving the use of blockchain, India can use it to create its own centralized cryptocurrency without any competition from other cryptos if it successfully bans other coins. Sukhi Jutla, co-founder of MarketOrders — a blockchain-based online jewelry marketplace — told Cointelegraph:“I think it’s more about the Indian government wanting to impose greater controls on how this new technology can be used, and they are clearly concerned with how it will impact their current financial system. The more controlling governments are around cryptocurrencies, the more fearful they are of the impact it will cause on their current financial systems.”Governments can either have a supportive and collaborative approach that allows innovation to occur or they can stifle and shut down progression and innovation if they remain too fearful of this technology, and it seems as though the Indian government may be taking the latter approach.Popular crypto influencer and trader Scott Melker, who is known by his Twitter name The Wolf Of All Streets, told Cointelegraph:“As of today, crypto and blockchain are now legal and encouraged in the country, but a 30% tax on all cryptocurrency trading hinders the growth. Following this disastrous tax policy, some exchanges have reported up to a 70% decline in trading activity. For now, it truly seems like India only has an interest in what blockchain can do for the country and not what Bitcoin can do for its citizens.”India’s struggle with crypto regulationsThe Indian finance ministry was first tasked with drafting a crypto bill in 2018, and the first draft copy was introduced in 2019, demanding a complete ban on all activities associated with cryptocurrencies. Since then, the government has changed its stance on crypto on several occasions, going from a blanket ban to regulating the crypto market as an asset class. However, none of the proposals have been finalized or introduced in parliament for discussion.The crypto ecosystem in India has managed to self-regulate for quite some time now. However, the hesitant stance of the Indian central bank, in addition to regulatory uncertainty, has made many crypto firms reconsider their future in the country.Recent: Madeira ‘embraces’ Bitcoin, and how its president met Michael SaylorNitin Agarwal, founder and chief revenue officer of FV Bank — an international digital bank — told Cointelegraph:“The job of regulators is difficult and is even more complex in the crypto space due to its inherent nature of being censorship-resistant coupled with grappling with the rapid pace of innovation. Regulators the world over are working hard on creating a regulatory framework that can be applied to digital assets and crypto. The Indian government’s approach is pragmatic in that they don’t want to over-regulate and see all users and companies move to a non-regulated or more lightly regulated jurisdiction.”He added, “The government is waiting to see a regulatory framework come out of the United States and European Union, which they can imbibe upon and take best practices to apply to the people of India.”While a majority of ministers in the ruling party have toed the line of the finance ministry, many opposition leaders have called for reconsideration of the flawed tax policy. They have also opposed the idea of banning crypto, claiming it would be similar to banning the internet.

Čítaj viac