US regulators push user ID requirements for stablecoin issuers akin to regulated banks

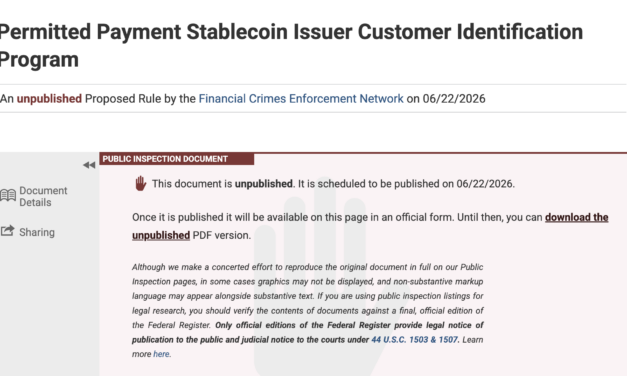

Several US government agencies responsible for financial regulation have issued a proposed rule as part of the implementation of stablecoin-focused legislation, pushing for similar identification guidelines for issuers as banks under federal law.The Federal Deposit Insurance Corporation (FDIC), Federal Reserve, Office of the Comptroller of the Currency (OCC), National Credit Union Administration and the US Treasury’s Financial Crimes Enforcement Network (FinCEN) on Thursday proposed that stablecoin issuers be treated as regulated financial institutions in regard to verifying users’ identities. The proposed rule comes as part of the implementation of the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, signed into law in July 2025.Source: Federal RegisterThe proposed rule, which will be open to public comment for 60 days after it is officially filed in the US Federal Register on Monday, is intended to address Anti-Money Laundering (AML) and Countering the Financing of Terrorism (CFT) requirements for stablecoin providers through the GENIUS Act. The minimum standards under the Bank Secrecy Act for financial institutions — potentially applied to stablecoin issuers under GENIUS — include “verifying the identity of any person seeking to open an account,” maintaining records of that information, and determining if the individual is a suspected terrorist or part of any terrorist organization.The agencies’ actions were the latest implementation related to GENIUS, largely championed by US stablecoin issuers. The law is expected to go into effect 18 months after it was signed or 120 days after federal authorities finalize regulations for implementation.Related: Banking group asks for more time to comment on US stablecoin billTreasury has already proposed AML and CFT requirements targeting illicit finance under GENIUS. In April, the FDIC suggested that rules providing insurance for corporate deposits of stablecoin issuers not extend to holders.GENIUS passed, CLARITY still being weighedAfter the passage of the GENIUS Act last year, the US Congress still has no defined timeline on addressing the Digital Asset Market Clarity (CLARITY) Act, a bill intended to redefine financial agencies’ roles in regulating and enforcing crypto rules. While many in the White House and Congress expect the bill to pass by the August recess, concerns voiced by Democrats over potential conflicts of interest from lawmakers and elected officials could slow progress.Magazine: The end of anon? AI could unmask crypto’s hidden identitiesCointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently.

Čítaj viac