Bitget pledges $10M for Fetch.ai ecosystem amid ChatGPT boom

The move comes amid a surge in popularity for artificial intelligence tools such as ChatGPT.

Čítaj viac

The move comes amid a surge in popularity for artificial intelligence tools such as ChatGPT.

Čítaj viac

The cash infusion reportedly followed Gemini attempting to get funding from outside investors without success.

Čítaj viac

BTC price faces pullback risks thanks to bearish on-chain movements and formidable technical resistance levels.

Čítaj viac

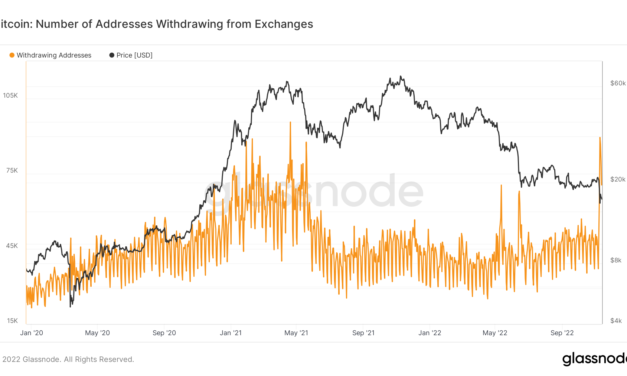

Bitcoin (BTC) investors are withdrawing funds from exchanges at a rate not seen since April 2021 with nearly $3 billion in Bitcoin withdrawn over the past seven days.New data from on-chain analytics firm Glassnode shows the number of wallets receiving BTC from exchange addresses hit almost 90,000 on Nov. 9.Exchange users wake up to self-custodyAmid ongoing turmoil over the bankruptcy of major exchange FTX, concerns have heightened among exchange users over security of funds.Commentators have upped advice to avoid custodial wallets and take control of cryptoassets, and regulators are increasing scrutiny of the crypto industry en masse.On-chain figures suggest that a large number of hodlers have opted for non-custodial wallets over the past week.The number of withdrawing addresses saw a huge spike on Nov. 9, this surpassing the daily highs for both May and June this year when BTC price action last saw significant downside pressure.For Nov. 12, the latest date for which data is available, withdrawing addresses still totaled over 70,000.Bitcoin exchange receiving addresses chart. Source: GlassnodeThe same Glassnode data gives an hourly average of over 3,000 withdrawing addresses over the seven days to Nov. 13.Bitcoin exchange receiving addresses chart. Source: Glassnode/ TwitterAnalysis: BTC reserves may not tell whole storyThe numbers tie in with what appears to be rapidly-declining BTC reserves across major trading platforms.Related: Bitcoin will shrug off FTX ‘black swan’ just like Mt. Gox — analysisWhile the velocity of the drop suggests that the true balance tally may be difficult to confirm at present, data from fellow on-chain analytics resource CryptoQuant puts overall exchange reserves at their lowest since February 2018.CryptoQuant tracks a total of 38 exchanges, including those with reported financial problems such as FTX and Kucoin.Bitcoin exchange reserve chart. Source: CryptoQuantAnother chart, this time from Coinglass, suggested 177,000 BTC in weekly withdrawals through Nov. 13 — a U.S. dollar value of around $3 billion at today’s price.BTC balance on exchanges chart. Source: CoinglassGlassnode senior analyst Checkmate nonetheless flagged three exchanges in particular with what he called “particularly weird” Bitcoin balance readouts — Huobi, Gate.io and Crypto.com.Concluding a dedicated thread into the topic, he noted that “Exchange balances are best estimate based on wallet clustering. They are more likely to be a lower bound than an overestimate.”“These fund flows between exchanges include both real customers + FTX/Alameda. Hard to separate, thus looking as relative-to-balance,” he added.Forecasting how the current scenario may play out, Michaël van de Poppe, founder and CEO of trading firm Eight, meanwhile said that the worst was likely not yet over.“Probably we’ll have more issues with exchanges coming weeks, but probably also a ton of gossip,” he told Twitter followers at the weekend. “Stay safe, be calm and don’t make emotional decisions. We’re in terrible territories, but crypto will come out of this stronger.”BTC/USD was trading at around $16,500 at the time of writing, data from Cointelegraph Markets Pro and TradingView showed.BTC/USD 1-hour candle chart (Bitstamp). Source: TradingViewThe views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Čítaj viac

In Celsius Network’s recent court filing, the billion-dollar centralized finance (CeFi) platform exposed more than 14,000 pages of customer identity and on-chain transaction data without user consent — a prescient reminder that privacy absent decentralization is no privacy at all.As part of its bankruptcy proceedings, CeFi lending giant Celsius Network disclosed names and on-chain transaction data of tens of thousands of its customers in an Oct. 5 court filing. While Celsius’ user base complied with standard Know Your Customer (KYC) procedures in order to open personal accounts with the CeFi platform, none consented to nor could have anticipated a mass disclosure of this scope or scale.In addition to doxxing the multi-million dollar withdrawals of Celsius founder Alex Mashinsky and chief strategy officer Daniel Leon just before Celsius’ bankruptcy announcement, the disclosure directed tens of thousands of CeFi users to reconsider what resolute privacy protections entail and how systems that incorporate any degree of trust or centralization stand to compromise those protections.To protect privacy, any degree of centralization or specialized authority that exchanges use in the future must eschew the bungled Celsius model. Otherwise, privacy will be rendered yet another false promise teased out in the fine print.Uncharted territoryWhile unsavory, at the very least, Celsius’ mass data dump points to more than an outright distrust of authority and opaque organizations. As per usual, at the intersection of on-chain finance and law, there’s a lot of gray area.An emergent and nascent industry, the blockchain space has already spun up a mess of unprecedented conflicts and disputes that neither existing legislation nor established case law has developed a reliable methodology to navigate. Even in the heavily nuanced legal environment of 2022, courts are not adequately prepared to uphold established legal principles in the on-chain domain.Related: Coinbase is fighting back as the SEC closes in on Tornado CashIn defense of their customers, Celsius’ legal representatives allege that they issued requests to redact private customer data from their disclosures. However, their requests were ultimately rejected by the court on the grounds that all Chapter 11 Bankruptcy proceedings require a complete and transparent “Creditor Matrix.” Obviously, such a bankruptcy rule was penned and passed several eras before the emergence of distributed on-chain lending protocols; a time when financial institutions did not have 14,000 pages worth of supposed creditors.To make matters more unclear, Celsius legal officials have also claimed that, as per Celsius’ terms of service, all user funds deposited in the platform essentially belong to Celsius. Thus, as a self-regarded de-facto owner of all customer deposits, Celsius’ public release of customer transaction data treads further into hazy legal territory as to the parameters that define ownership — and, therefore, privacy protections — in the on-chain space. Whatever the case, Celsius’ customers have permanently lost their privacy. The only sure verdict is that there can be no certainty in depending on an unprepared legal system to uphold privacy rights in fluid and uncharted territory.Celsius isn’t aloneAlthough dramatic, Celsius’ meltdown is only the most recent in a stint of CeFi industry bankruptcies. The platform’s billion-dollar deficit presented in bankruptcy filings has been much less the exception than the rule.Once one of crypto’s dearest and most powerful CeFi platforms, Celsius’ rise and downfall serve as a painful reminder to crypto critics and advocates alike that a core team can become a singular point of failure at any time. And further, centralized KYC procedures always carry some risk of exposure in legal proceedings.The predicament tens of thousands of innocent crypto investors now face points to a much broader principle: that privacy cannot be truly conferred nor absolutely protected within the confines of a centralized system. Even with the best intentions in mind, professionals on both sides of the court have little legal precedent to draw from as they navigate the novel and perplexing territory.Related: Government crackdowns are coming unless crypto starts self-policingAs on-chain data analytics become more sophisticated, hackers more conniving and personal data ever more valuable to marketing agencies and authorities, privacy-conscious individuals must exercise the utmost prudence in determining which crypto platforms best align with and protect their interests.After all, Google, Meta, and the rest of the Web2 platforms that the crypto community has since dismissed as exploitative and archaic are about as private as Celsius and its CeFi counterparts. Each provides privacy as a service. Meanwhile, its users’ search histories, account information and browsing preferences are private to almost everyone — except, of course, the platform itself. As Celsius’ bankruptcy proceedings have proven, even the most well-intended custodians are not a sufficient substitute for decentralized architecture.The true promise of systems built on blockchain is that what they confer, be it asset ownership, scarce monetary units or permissionless contracts, cannot be regulated, erased or modified on a whim. Their constitutions are written in code. Any and all modifications are coordinated and executed by decentralized autonomous organizations ( DAOs). There is no trust between counterparties, only a shared belief in the permanence of principle and the wisdom of the collective.In the same way, privacy has been a prerequisite for personal freedom and self-expression since time immemorial, decentralization is today a prerequisite for privacy online — and, to that end, on-chain.Alex Shipp is the chief strategy officer at Offshift, where he contributes to platform tokenomics, produces content and conducts business development on behalf of the project. In addition to his industry role as an expert in private decentralized finance (PriFi), he has also served as a writer at the Elastos Foundation and as an elected ecosystem representative on the Cyber Republic DAO.This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice. The views, thoughts and opinions expressed here are the author’s alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

Čítaj viac

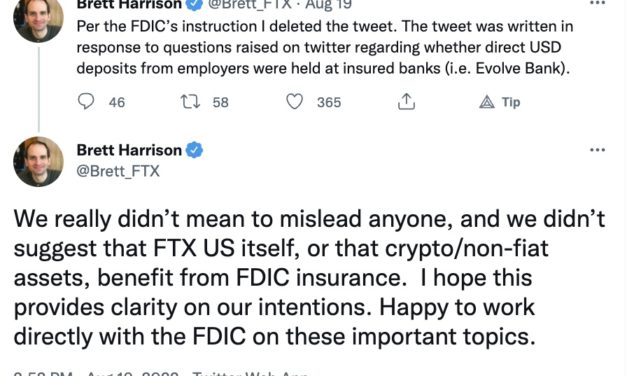

In a cease-and-desist letter to fast-growing crypto exchange FTX, the Federal Deposit Insurance Corporation (FDIC) shed light on a now-deleted tweet from the exchange’s president, Brett Harrison, and issued a stark warning over the company’s messaging.Harrison’s original tweet said, “Direct deposits from employers to FTX US are stored in individually FDIC-insured bank accounts in the users’ names.” He added, “Stocks are held in FDIC-insured and SIPC [Security Investor Protection Corporation]-insured brokerage accounts.”Although Harrison stewarded FTX to its best-ever year in 2021, increasing revenue by 1,000%, the firm now faces the unenviable prospect of running afoul of a powerful government agency.In an attempt to clarify the situation to his 761,000 Twitter followers, Brett said, “Clear communication is really important; sorry! FTX does not have FDIC insurance (and we’ve never said so on website etc.); banks we work with do. We never meant otherwise, and apologize if anyone misinterpreted it.”But it seems the statements made on Twitter by Harrison in response to the FDIC cease-and-desist letter over “false statements” were factually correct: User funds are held at banks insured by the FDIC. Related: FDIC–FTX spat is another reason for investors to get their funds off exchangesHis original communications were construed as if the funds were themselves insured, which they’re not. Either way, firms are not allowed to mention a relationship with the FDIC unless there is a direct link and the correct language is used to clearly describe it.This was an error in messaging on the part of FTX. A mistake was definitely made, inciting perhaps rightful outrage from the community. They may have taken this to believe they were transacting with an insured exchange, which could ensure catastrophic failure would not lead to loss of funds, after all. BREAKING: #FDIC just issued a cease and desist letter to #FTX for misleading statements, such as client deposits being insured by FDIC. It is good that finally FDIC is doing something about misleading and fraudulent #crypto firms. pic.twitter.com/vl0JDtM6LY— WallStreetPro (@wallstreetpro) August 19, 2022However, it’s almost certainly not the case that there were sinister motives. Harrison wrongfully communicated the relationship between FTX and the FDIC and was swiftly corrected before he immediately moved to rectify the official FTX position on deposit insurance. Nothing more than a storm in a teacup, one might say. The FDIC issued similar cease-and-desist letters to four other companies on the same day for the exact same reason: implying there is deposit insurance when none exists. It begs the question of whether this is really a result of nefarious actions.Companies like Celsius do represent a threat to the industryThere is plenty of chagrin to throw around the crypto space. Take Celsius, for example. It’s fair to argue the company’s policy terms and conditions did not align with what it implied through its messaging. Around 1.7 million customers were left in the lurch with little idea of whether they would be able to retrieve their funds.Rug pulls, scams and fraud thrive in a low-regulation industry, and indeed, this means there are plenty of villains out there to direct public anger at.When it comes to FTX, there is an observable mission to do serious business and foster legitimacy in the world of cryptocurrencies. This is an exchange very much on the ascendancy, attracting and retaining over 1 million users and trading around $10 billion in daily volume as of February 2022.Related: Binance vs. FTX: CZ calls out ‘bad players’ for crypto exchange jittersConsumers should not distrust or dislike big players just because they are big. These firms are likely the harbingers of mainstream adoption, which is surely the aim of crypto. Self-custody is obviously the safest way to store funds, but not everyone can ensure they mitigate all associated risks. Their best bet is an exchange like FTX.Regulators should become more proactive and less reactiveA focus on the experience of the end-user is perhaps murky when it comes to cryptocurrencies. Volatility means retail investors most often lose money, while tracing transactions can be difficult, and the government wants to retain the ability to do so.Right now, it seems regulators can only step in after an egregious mishap must be corrected. While crypto is seeping into the mainstream, overall public perception seems to be negative, and mass adoption will only be possible years into the future.Regulations working in tandem with the emergence of mainstream solutions that provide a genuinely great user experience could be key. Policymakers have had plenty of time to prepare for a future with blockchains underpinning vast swathes of real-world applications. Once the technology matures to the point that it becomes as simple as using the internet, the prospect of intelligent regulatory oversight becomes far more likely.Toby Gilbert is the CEO of Coinweb.io, a cross-chain computation platform. He graduated from London’s Global University (UCL) before starting a career in the tech and telco spaces. He invested in and exited three telecommunications companies in Europe, Africa and Asia before joining Coinweb in 2018. He also co-founded the Blockfort and OnRamp DeFi projects.The opinions expressed are the author’s alone and do not necessarily reflect the views of Cointelegraph. This article is for general information purposes and is not intended to be and should not be taken as legal or investment advice.

Čítaj viac

Unregistered cryptocurrency exchanges operating in South Korea could see their services grind to a halt as the Korea Financial Intelligence Unit (FIU) takes action against 16 foreign-based firms.The FIU has notified its investigative authority that 16 virtual asset service providers have been carrying out business without the necessary registrations. Major exchanges, including the likes of KuCoin, Poloniex and Phemex, were listed alongside 13 other exchanges that are set to be hamstrung by the FIU.All 16 exchanges have purportedly engaged in business activities targeting domestic consumers by offering Korean-language websites, running promotional events targeting Korean consumers and providing credit card payment options for cryptocurrency purchases. These activities all fall under the Financial Transactions Report Act.The FIU has already taken action against the unregistered exchanges by reporting the violation of registration duties and intends to inform their counterparts in the respective countries that the businesses operate. Unregistered entities face five years in prison, a fine of ~$37,000 and a potential ban on future registration in the country.Related: South Korea’s small crypto exchanges face increasing regulatory heatA request has also been submitted to the Korea Communications Commission and the Korea Communications Standards Commission to block domestic access to the websites of the exchanges in question.Credit card service providers have been requested to identify and block cryptocurrency purchases made with credit cards. The FIU has also issued a requirement to registered exchanges in the country to suspend transactions from the 16 unregistered companies in an effort to curb transfers to other platforms. South Korea’s Financial Services Commission announced a deadline for local and foreign-based, cryptocurrency-related businesses to register with the relevant authorities in July 2022. Sept. 24 is the due date for companies to register before they are liable to face criminal prosecution and the prospective fines and penalties previously mentioned.While the FIU takes aim at unregistered exchanges, the FSC has vowed to expedite the review of 13 different bills relating to cryptocurrencies under consideration of the National Assembly. Efforts are being made to produce legislation that has balanced approach to blockchain development, investor protection and market stability.

Čítaj viac

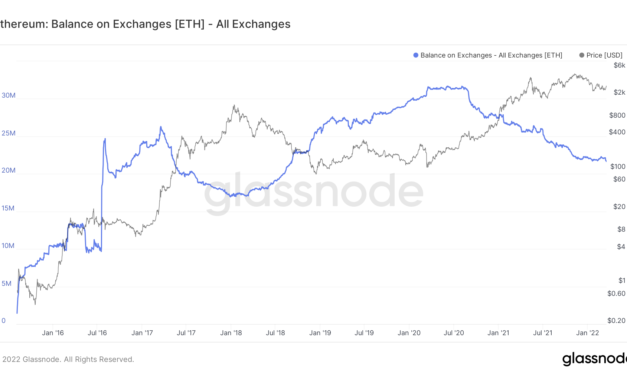

The amount of Ethereum’s native token Ether (ETH) kept with crypto exchanges has fallen to its lowest levels since September 2018, signaling traders’ intention to hold the tokens in hopes of a price rally in 2022.Notably, nearly 550,000 ETH tokens — worth around $1.61 billion — have left centralized trading platforms year-to-date, according to data provided by Glassnode. The massive outflow has reduced the exchanges’ net Ether balance to 21.72 million ETH, down from its record high of 31.68 million ETH in June 2020.Ethereum balance on all exchanges as of March 18, 2022. Source: GlassnodeBiggest weekly ETH outflow since October 2021Interestingly, over 30% of all Ether’s withdrawals from exchanges witnessed in 2022 appeared earlier this week, data from IntoTheBlock shows. In detail, over 180,000 ETH left crypto trading platforms on March 15, bringing the weekly outflow’s worth to a little over $500 million as of March 18.Ethereum net exchange flows. Source: IntoTheBlockChainalysis data showed similar readings, revealing that Ether tokens could have left exchanges this week at an average of about 120,000 units per day, a bullish signal. Excerpts:”Assets held on exchanges increase if more market participants want to sell than to buy and if buyers choose to store their assets on exchanges.”IntoTheBlock provided a similar upside outlook while citing a fractal from October 2021 that saw the Ether’s price rising by 15% ten days after the Ethereum network detected massive ETH withdrawals from centralized crypto exchanges.Ethereum supply crunch underwayThe increase in Ether withdrawals from exchanges this week coincided with about 190,000 ETH moving into Lido’s “stETH liquid staking” pools, IntoTheBlock noted.To recap, Lido is a non-custodial staking service that enables users to overcome challenges associated with staking on the Ethereum 2.0 Beacon Chain, including the requirement of staking a minimum of 32 ETH or its multiples. Furthermore, Lido proposes to solve the capital efficiency problem by issuing stETH, the tokenized version of staked ETH.The last 30 days showed Ether holders adding over 1 million ETH into the Ethereum 2.0 contract. And as the protocol prepares to switch completely to proof-of-stake in summer — in the wake of its “Merge” earlier this week on the Kiln testnet — the probability of more Ether tokens going out of active supply has increased.Lol. No one told anon that there’s going to be a liquidity squeeze in newly minted Ether in a few months. No newly minted Ether will enter circulation between the Merge (Juneish) and Shanghai (Decemberish). I’d text them but I don’t even have their number. You got it? Poor anon.— superphiz.eth (@superphiz) March 16, 2022ETH price rebound continuesThe bullishness surrounding Ethereum’s switch to proof-of-stake has prompted Ether to enter a rebound mode this week. Related: Vitalik Buterin talks crypto’s perils in Time Magazine interviewIn detail, ETH’s price rallied by more than 17% week-to-date to nearly $3,000. Interestingly, the upside retracement originated at a technical level — rising trendline support with a recent history of limiting Ether’s bearish outlooks, as shown in the chart below.ETH/USD daily price chart. Source: TradingViewNonetheless, as Cointelegraph covered earlier, Ether could pare its gains owing to another technical level, this time a falling trendline resistance that has also been instrumental in capping its upside attempts since January 2022.Together, these trendlines appear to have formed a continuation pattern called a symmetrical triangle, indicating that Ether will most likely go in the direction of its previous trend, i.e., down. For now, ETH could fall back toward the triangle’s support trendline on a pullback from its resistance one. The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Čítaj viac

Bitcoin (BTC) jumping to $39,000 has already activated large-volume investors this week, the latest data shows.Analyzing whale behavior, on-chain monitoring resource Whalemap revealed accumulation underway at levels above $36,000.This week’s BTC price “triggered” whalesIdentifying clusters of whale bids, Whalemap uncovered what appears to be renewed market confidence among those with some of the largest BTC balances — between 100 BTC and 10,000 BTC.“Recent prices triggered whales to accumulate Bitcoin,” researchers summarized on Twitter Tuesday.According to cluster data, whales now own 330,000 BTC bought at spot prices between $36,000 and $38,000.Whale wallet accumulation annotated chart. Source: Whalemap/TwitterOverall, the portion of the BTC supply per whale wallet is now at its highest in a decade, data from on-chain analytics firm Glassnode uploaded to Twitter by popular account Priced in Bitcoin shows. This comes despite the vastly larger Bitcoin user base compared to the largest cryptocurrency’s early days. Bitcoin supply per whale vs. BTC/USD chart. Source: Priced in Bitcoin/TwitterTrader and analyst William Clemente, meanwhile, described last week’s whale activity as “fairly heavy” buying.Exchanges see new influx of BTC this weekendThe results run in contrast to a decreasing buying trend, which began in the second half of January.Related: Bitcoin market cap dominance hits 2-month high as altcoins struggleAs Cointelegraph reported, exchanges returned to seeing greater outflows than inflows in recent weeks, despite spot price action putting in lower lows.In the past few days, however, exchange users have conversely sent BTC to their accounts as BTC/USD has risen to its highest levels in two weeks.The 21 platforms monitored by on-chain analytics firm CryptoQuant saw their balance increase from 2.357 million BTC on Jan. 29 to 2.377 million BTC on Jan. 31, the latest date for which data is currently available.Bitcoin exchange reserves vs. BTC/USD chart. Source: CryptoQuantWhales may not actively use exchanges for larger buys, particularly if they are in a position to perform over-the-counter trades or purchase coins directly from miners.

Čítaj viac

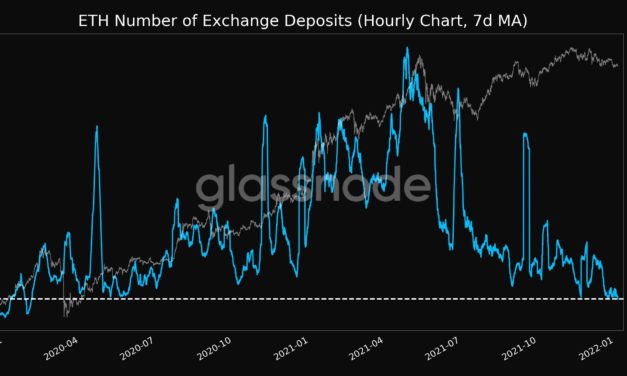

Ethereum’s native token Ether (ETH) has plunged by more than 20% after establishing its record high at around $4,867 on Nov. 10, 2021. Nonetheless, the sharp price pullback does not mean ETH can’t pursue a new record high in the next few months, as several widely-tracked technical, macroeconomic and on-chain indicators suggest. One of these indicators envisions Ether’s price reaching $5,000 in the first quarter of 2022 while others look are poised to support the bullish bias.ETH price painting falling wedgeEther’s recent price correction is painting a potential classic bullish reversal pattern known as “falling wedge.”In detail, falling wedges begin wide at the top but contract as the price moves lower. As a result, the price action forms a conical shape that trends lower as the reaction highs and reaction lows converge. Traders realize a bullish bias only after the price decisively breaks above the wedge’s resistance.As a result, expectations remain high that the ETH price would break above its falling wedge resistance in the coming sessions. In doing so, it would rise by as much as the maximum distance between the wedge’s upper and lower trendline when measured from the breakout point. Literally unchanged…$ETH is going to $5k pic.twitter.com/11mAQiJxJS— Kong Trading (@KongBTC) January 4, 2022That roughly puts the price target for Ether at $5,000.ETH deposits to exchanges dropTraders typically move their tokens to exchanges when they intend to sell/trade them for either fiat, stablecoins or other cryptocurrencies. Generally, a higher number of transactions made to crypto trading platforms reflects a high selling sentiment in the market. Conversely, if the token transactions plunge, they show a strong holding sentiment in the market.Data collected by blockchain analytics service Glassnode show that the number of on-chain Ether deposits to exchanges dropped to its 23-month low on Jan. 3.ETH number of exchange deposits. Source: GlassnodeAdditionally, another Glassnode metric that tracks the number of Ether addresses sending ETH to exchanges also reported declines over the last 30 days, the same period that saw the ETH/USD rate dropping nearly 11%.Ethereum number of addresses sending to exchanges. Source: GlassnodeMeanwhile, the total Ether balance across all the exchanges has been in a downtrend since Aug. 2020, suggesting that ETH investors are in it for the long haul as its price rose from nearly $400 to a little over $3,800 in the same period.Ethereum balance on exchanges. Source: GlassnodeCheap money here to stay? Ether’s $1,000-plus plunge from Nov. 2021 to date came majorly in the wake of the Federal Reserve’s hawkish turn.The U.S. central bank decided to accelerate the unwinding of its $120 billion a month asset purchase program, followed by three rate hikes in 2022 from its near-zero levels, to stem rising inflation. Its loose monetary policy was one of the primary catalysts behind similar price rallies across Ethereum, Bitcoin (BTC) and other crypto markets.ETH/USD and BTC/USD weekly price chart. Source: TradingViewBut the Fed’s efforts to tame inflation from its current 6.8% level with three rate hikes may not impact Bitcoin and Ethereum prices in the long run. For example, Antoni Trenchev, managing partner of crypto lender Nexo believes that cheap money is here to stay. “The No. 1 influencing factor for Bitcoin and cryptocurrencies in 2022 is central bank policy,” he told Bloomberg. He added:“Cheap money is here to stay, which has huge implications for crypto. The Fed doesn’t have the stomach or backbone to withstand a 10%–20% collapse in the stock market, along with an adverse reaction in the bond market.”Hungarian-born billionaire Thomas Peterffy also said that investors should allocate at least 2%–3% of their net portfolio to cryptocurrencies like BTC and ETH in case the fiat money “goes to hell.” Related: More billionaires turning to crypto on fiat inflation fearsAdditionally, Bridgewater Associates founder Ray Dalio revealed that he has been holding BTC and ETH in his portfolio against the risks of cash devaluation led by higher inflation.The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph.com. Every investment and trading move involves risk, you should conduct your own research when making a decision.

Čítaj viac