Tento príspevok bol pôvodne publikovaný na stránke https://cointelegraph.com/news/drawbacks-of-centralization-moscow-stock-exchange-remains-offline-amid-ongoing-russo-ukrainian-war a autorom článku je Cointelegraph By Zhiyuan Sun. Tento článok je iba kópia originálneho článku.

https://images.cointelegraph.com/images/840_aHR0cHM6Ly9zMy5jb2ludGVsZWdyYXBoLmNvbS91cGxvYWRzLzIwMjItMDMvZTAzMjc4MDMtOTZhNi00ZjIzLTk2NTEtNmFkYzJmMDI2MjIxLmpwZw==.jpgAs reported by local news outlet tass.ru, the Central Bank of Russia once again suspended trading on the nation’s leading Moscow Stock Exchange (MOEX) on Wednesday, and will not open the exchange on Thursday. Trading on the MOEX has been halted since Feb. 25, after Russia launched its ongoing military occupation of Ukraine. On a monthly basis, the exchange’s index has lost over 34% of its value (not adjusted for inflation), as Western leaders imposed crippling sanctions on Russia in response to the conflict.

In addition, MOEX’s main website has been knocked offline since Monday, with Ukraine’s IT Army allegedly taking credit for the “hack.” Meanwhile, Russia’s Saint Petersburg Stock Exchange (SPB) also remains closed but will open for limited trading tomorrow. In the meantime, the Dow Jones Russia GDR Index, which tracks the value of Russian stocks listed on the London Stock Exchange, has lost 93% of its value in the last five trading days, implying disastrous losses ahead when Russian markets open.

Theoretically, whether centralized or decentralized exchanges (CEXs or DEXs), cryptocurrency exchanges would be free from such intervention. In addition to their sheer numbers, CEX servers can be spread out worldwide or do not disclose their server locations. Governments can, therefore, ban exchanges within their borders but cannot enforce a ban on crypto trading. As for DEXs, their peer-to-peer nature typically enables anyone with an internet connection to link their wallets and swap crypto, making it difficult to enforce any type of ban altogether.

While Russian financial institutions have the means to weather a stock market catastrophe, the same cannot be said for everyday Russians. More than 17 million retail investors trade on the MOEX alone, and together, retail investors account for more than 40% of the country’s equity trading volume. Coupled with a sharp decline in the ruble’s value, it is likely the retail investor community in Russia, such as that of pensioners and retirees, will suffer severe losses to their savings when markets open.

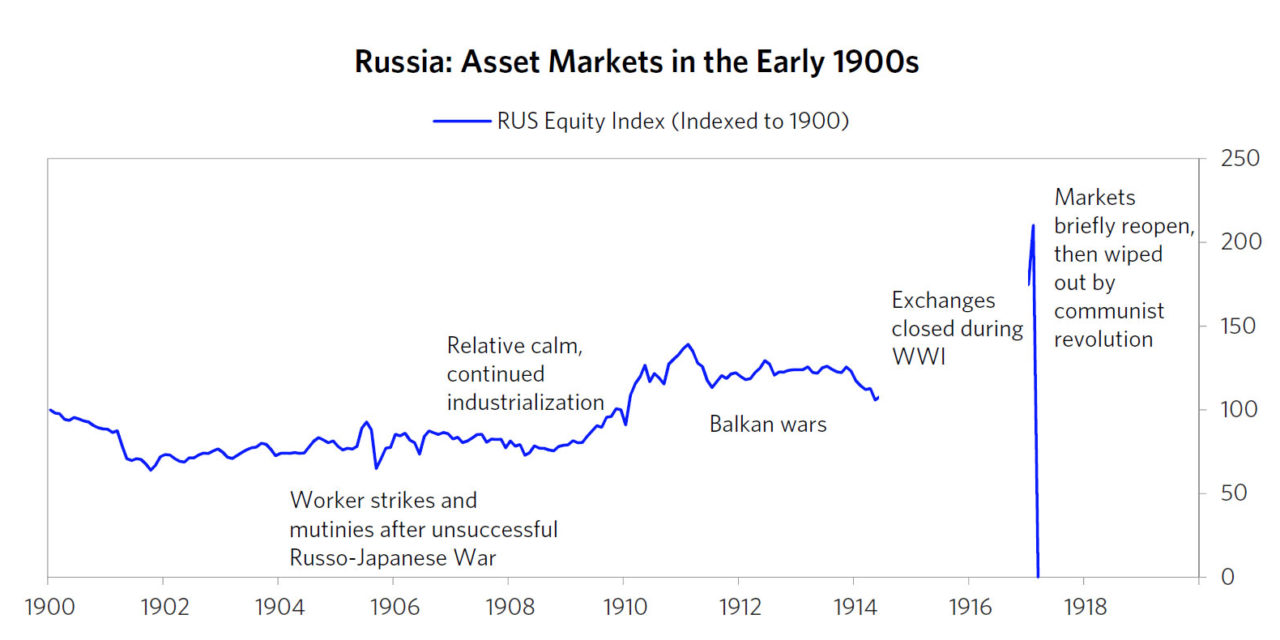

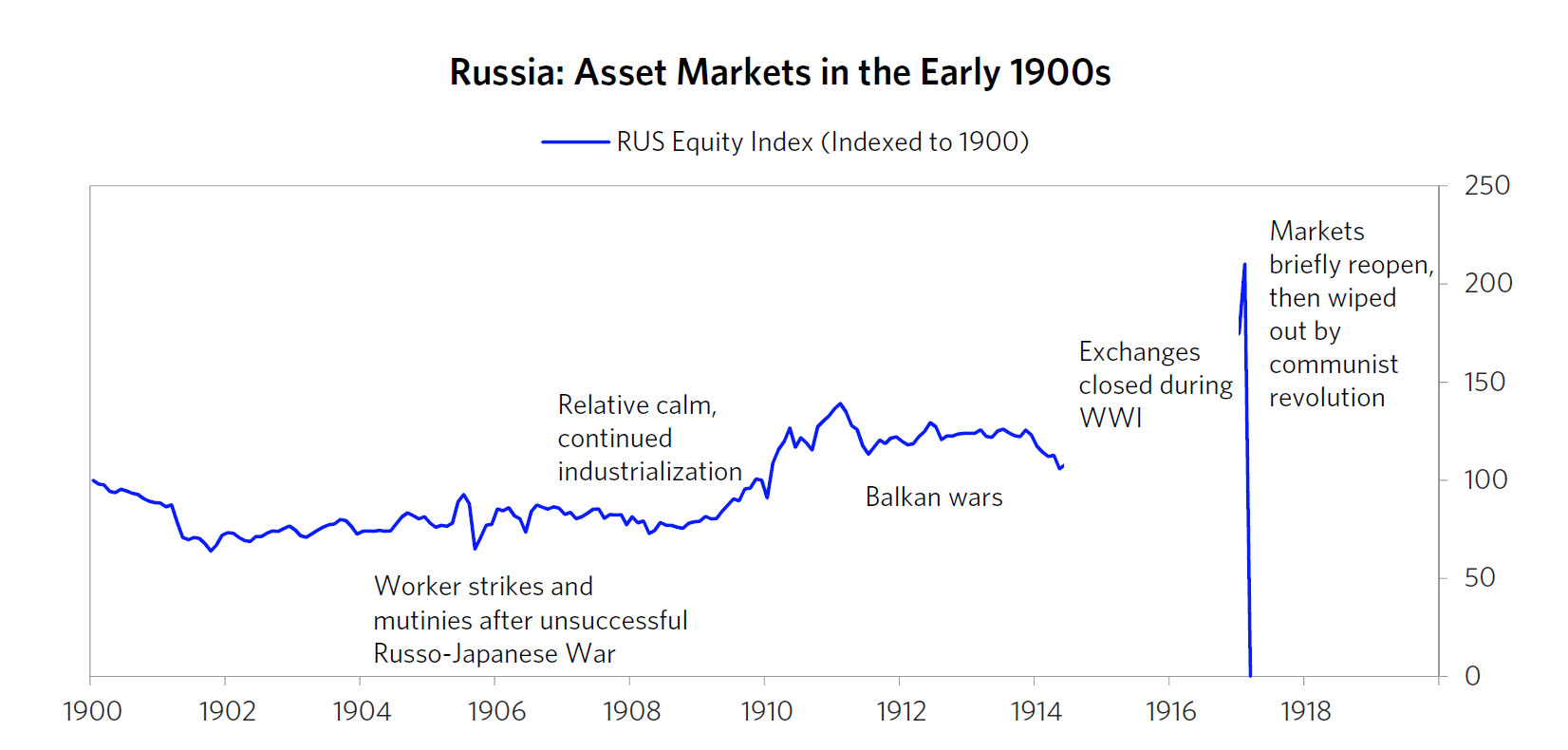

But perhaps there is no better path to understanding the dangers of centralized control over capital markets than through the archives of the SPB, itself. During the imperial era, the SPB was one of the top-performing stock markets in the entire world, even besting the performance of the New York Stock Exchange for much of the latter half of the 19th century. However, trading on the SPB halted with the outbreak of World War I. They opened briefly after the outbreak of the Russian Revolution in 1917. But when the Bolsheviks took over, the SPB was closed down for good, with investors who couldn’t sell in time losing every single kopek (Russian penny).

Russian equity index of the 1900s | Source: SNB & CHF (Author’s note: The “spike” in 1917 resulted from hyperinflation during the Russian Revolution, where stock prices “went up” simply due to the printing of large-denomination ruble notes, in part, to fund military expenditures. Meanwhile, their “real” value as compared to foreign currencies, plunged)

{kind=link}