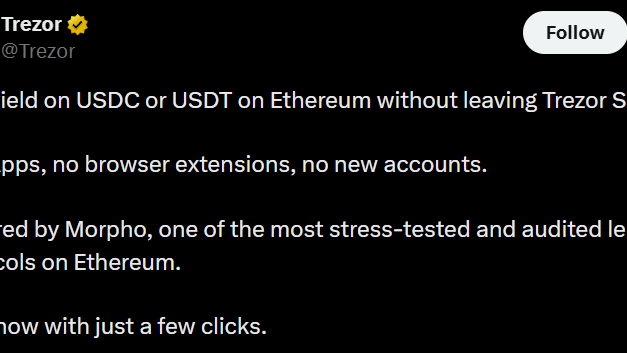

Trezor adds native USDt, USDC yield via Morpho integration

Trezor has integrated native stablecoin yield functionality into Trezor Suite, the hardware wallet provider’s desktop and mobile application, in a move that could make earning yield on stablecoins more accessible to users who have traditionally avoided decentralized finance due to its complexity and security risks.Announced on Thursday, the feature comes through an integration with Morpho, a decentralized lending protocol built on Ethereum. The integration allows users to deposit USDt (USDT) and USDC (USDC) into pre-selected Morpho vaults directly through Trezor Suite without connecting external wallets or using separate DeFi applications.According to Trezor, deposits, withdrawals and reward claims are signed directly on users’ hardware wallets through the company’s clear-signing interface, which displays transaction details in human-readable form on the device screen.Source: TrezorAt launch, Trezor selected two Morpho vaults curated by Steakhouse Financial — USDC Prime and USDT Prime. The company said yield is generated from borrowing demand on Morpho rather than token incentive programs.Trezor is one of the largest crypto hardware wallet providers and is widely considered the second-largest player in the market behind Ledger.Wallet providers have recently been making a broad push to incorporate decentralized finance functionality directly into custody products while reducing the complexity traditionally associated with DeFi protocols. Ledger already offers native stablecoin yield through Ledger Live using Kiln-powered integrations with protocols including Morpho, Aave and Compound.Related: ERC-7943 author says institutions can’t play DeFi’s ‘pirate game’Stablecoin yield draws growing interest — and scrutinyStablecoin yield strategies have become one of the fastest-growing use cases in DeFi, allowing users to earn returns on dollar-pegged assets by lending them through onchain protocols.According to CoinMarketCap data, USDC yields can vary widely across platforms and market conditions, with some protocols offering double-digit annual returns. Supporters say stablecoin yield products offer crypto holders a way to generate passive income.However, the strategies also carry risks, including smart contract vulnerabilities, liquidity issues and exposure to centralized stablecoin issuers or counterparties.Ethereum co-founder Vitalik Buterin recently drew a distinction between decentralized finance and many of the yield-focused stablecoin products currently on the market. In a recent post, Buterin said that many “USDC yield” strategies remain heavily dependent on centralized issuers while failing to adequately address counterparty risk.Source: Vitalik ButerinButerin proposed two alternative models that he said align more closely with DeFi’s decentralized ethos: Ether-backed algorithmic stablecoins and overcollateralized real-world asset-backed stablecoins.Related: Crypto Biz: Institutions tighten their grip on Bitcoin, AI and prediction markets

Čítaj viac