Philippines’ digital transformation could make it a new crypto hub

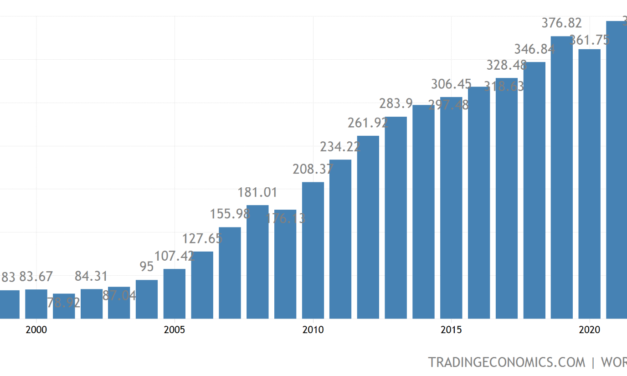

Binance, the cryptocurrency exchange, has recently acquired a virtual asset service provider (VASP) license from the Bank of Spain in order to operate in the country. In its ambitious expansion plans that the cryptocurrency exchange is persisting despite the global jump and market slump in the cryptoverse, there is another country that Binance is looking toward — the Philippines.In June, the CEO of Binance, Changpeng Zhao, stated in a press briefing in Manila that the exchange is looking to obtain a VASP license in the Philippines. In addition to the VASP, Binance wants to get an e-money issuer license from the central bank of the country, Bangko Sentral ng Pilipinas (BSP). While the former license would allow the platform to offer trading services for crypto assets and the conversion of these assets to the Philippines, the latter will allow it to issue electronic money.The Philippines is the world’s 36th largest economy in the world by nominal GDP and the third-largest in Asia, according to data from the World Bank. Despite its small size, the country is considered to be one of the fastest-growing economies in the world due to it being newly industrialized, thus marking a distinctive shift from agriculture to services and manufacturing.Philippines gross domestic product in U.S. dollars 1997–2001. Source: Trading EconomicsCryptocurrencies are extremely popular in the Philippines due to the economic shift that the country went through when digital assets began to gain popularity. A recent survey has revealed that the Philippines ranks 10th in cryptocurrency adoption, with over 11.6 million Filipinos owning digital assets.This is also evidenced in the fact that according to data from ActivePlayer.io, 40% of all the players of the popular play-to-earn (P2E) game Axie Infinity were from the Philippines. In fact, the game has also been a financial game-changer for many citizens in the country.Related: How blockchain games create entire economies on top of their gameplay: ReportCointelegraph spoke with Omar Moscosco, co-founder of AAG Ventures — a P2E guild based in the Philippines — about the potential the Philippines holds for the mass adoption of digital assets. He said, “The Philippines is home to a large unbanked and underbanked population with some 66 percent of this total population having no access to traditional banking services or similar financial organizations.”He added that COVID-19 sparked a digital transformation in the country, saying:“The Philippines registered the highest number of first-time users of digital payment methods at 37 percent. The regional average was 15 percent. As such, digital payments made up 20 percent of total financial transactions in the country in 2020, an increase from 14 percent in 2019. Also, in 2020, e-money transactions totaled 2.39 trillion PHP (US$46.5 million), an increase of 61 percent compared to 2019.”Jin Gonzalez, chief architect of Oz Finance — a decentralized finance (DeFi) service provider based in the Philippines — told Cointelegraph about the impact the entry of Binance in the country would entail for the market. He said, “Binance already receives a large amount of Philippine peso volume for its peer-to-peer (PHP/USDT) service. It is also the exchange of choice for Filipinos due to the favorable rates it charges versus local service providers. Getting a BSP license will only legitimize its operation and strengthen its position in the market.”However, global concerns have begun to emerge around the Anti-Money Laundering (AML) and Combating the Financing of Terrorism (CFT) frameworks that companies with VASP licenses use. The central bank of Ireland has published a bulletin for VASPs that is aimed at assisting applicant firms to strengthen their VASP registration application and their AML/CFT frameworks accordingly. This development was good for the growing ecosystem, as it addresses concerns that would inevitably arise when considering the integration of digital assets into the existing financial ecosystem and the economy. At the same time, Hong Kong introduced a licensing regime for VASPs in June this year, which imposes statutory AML/CTF requirements for companies that wish to operate in the nation.Central government keen to push use casesThe regulatory landscape of the Philippines is still in a fairly nascent stage as there is no strict restrictive regulation for both businesses and individuals at the moment. In fact, the government of the country, in tandem with its central bank, seems keen to adopt blockchain technology and implement its use cases in various sectors of the economy. Gonzalez said:“At the current moment, BSP regulation is in place, but SEC regulation has yet to pass. Regardless, the Philippines has an open position on digital assets, and its intent to regulate is intended to balance investor protection with promoting the advancement of the technology. PH regulators, especially the Central Bank, maintain a progressive stand on the adoption of digital assets.”Earlier this year, in May, the Philippines government’s Department of Science and Technology started a blockchain training program for researchers in the department. Through the training program, the government is looking to adopt blockchain in areas such as healthcare, financial support, emergency aid, issuance of passports and visas, trademark registration and government records, among others.Cliffs at El Nido in the Philippines. Source: TudernaThe Philippines-based UnionBank has also launched a payments-focused stablecoin pegged to the Philippine peso that aims to drive financial inclusion in the country. It attempts to link the main banks of the country to rural banks and bring financial access to previously unbanked parts of the country. Gonzalez said:For the time being, it seems content to observe how bank-issued stablecoins (such as PHX by UnionBank) will bring forward financial inclusion.However, even with the openness of the government, there are entities keeping a keen eye out for irregularities in the way digital asset companies are operating. The local policy thinktank Infrawatch PH has sent a letter to the Philippines’ Department of Trade and Industry (DTI) asking them to conduct an investigation against Binance for promotions in the country without having a proper permit for the same.The DTI responded to this letter, putting the ban out of the question by stating that it has set no clear guidelines for the promotion of digital assets.CBDC launch could be a gamechanger for the countrySince a majority of the citizens in the Philippines are unbanked and thus operate in a fairly unregulated manner in matters like taxation, the introduction of a central bank digital currency (CBDC) into the economy could be a major step in the digital transformation that the country is currently undergoing.Moscoso said, “CBDCs can take advantage of mobile technologies to provide increased access to financial services to rural households and other segments that are underserved by the current banking system. The central bank expects that at least half of the payments would eventually be made digitally by 2023.”Related: Crypto in the Philippines: Necessity is the mother of adoptionHe added that around 70% of adults would be using a digital account for transactions by this time, which allows consumers to have additional options that can make them steer away from loan sharks.Despite the current bear market, the Philippines still has a forward-thinking perspective about the adoption of digital assets and blockchain-based business models. This outlook puts the country in a good spot, with the potential to become a cryptocurrency hub.

Čítaj viac