Finance Redefined: Hacker bungles DeFi exploit, dYdx's decentralization goals, and more

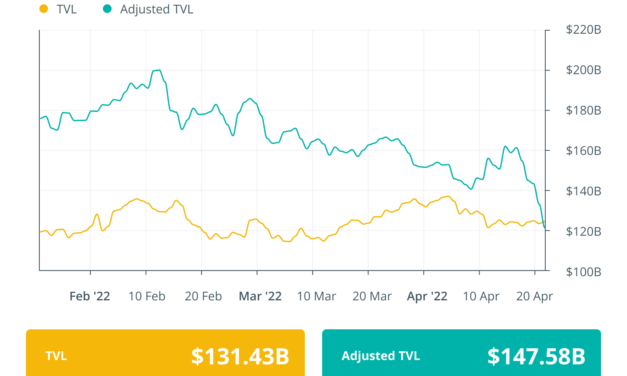

The decentralized finance (DeFi) ecosystem was filled with ups and downs —mostly the latter— this week, with two very distinct hack attempts and a heartbreaking departure of a DeFi veteran. In this week’s newsletter, we will also look at derivative exchange dYdX’s plans to go fully decentralized by the end of the year. The price momentum of the DeFi tokens remained neutral, with several tokens registering a bullish surge. However, the market volatility meant many of them couldn’t hold onto those gains.Hacker bungles DeFi exploit: Leaves stolen $1M in contract set to self destructIn a rare comedic bungle among DeFi exploits, an attacker has fumbled their heist at the finish line leaving behind over $1 million in stolen crypto. Blockchain security and analytics firm BlockSec shared on Thursday that it had detected an attack on a little-known DeFi lending protocol called Zeed, which styles itself a “decentralized financial integrated ecosystem.”The attacker exploited a vulnerability in the way the protocol distributes rewards, allowing them to mint extra tokens which were then sold, crashing the price to zero but netting just over $1 million for the exploiter.Continue readingDerivatives exchange dYdX to become ‘100% decentralized by EOY’Ethereum layer-2-based crypto derivatives trading platform dYdX has vowed to become “100% decentralized by EOY” via the protocol’s v4 update.At present, only certain components of dYdX are decentralized including its Ethereum smart contracts, governance and staking. However, its “order book and matching engine” are managed by dYdX Trading Inc. — the team that developed the platform.Continue readingAndre Cronje sees a ‘necessity for regulation’ ahead of crypto’s new eraAndre Cronje, former Fantom Foundation technical adviser and Yearn.finance founder, resurfaced on Monday via Medium after announcing his departure from the DeFi and crypto space last month. In a post titled “The rise and fall of crypto culture,” Cronje expressed his lamentations of crypto culture as he called for increased regulation and legislation in the industry.The top highlight in the post is the phrase: “Crypto culture has strangled crypto ethos.” According to Cronje, he has a “disdain” for crypto culture but a “love” for crypto ethos. He explained that the culture, which prioritizes “wealth, entitlement, enrichment and ego,” has suppressed the principles of “self-sovereign rights, self custody and self-empowerment.” Continue reading Beanstalk Farms loses $182M in DeFi governance exploitCredit-based stablecoin protocol Beanstalk Farms lost all of its $182 million collateral from a security breach caused by two sinister governance proposals and a flash loan attack.The problem with the protocol was seeded by suspicious governance proposals BIP-18 and BIP-19, which were issued on Saturday by the exploiter, who asked for the protocol to donate funds to Ukraine. However, those proposals had a malicious rider attached to them that ultimately created the sinkhole of funds from the protocol, according to smart contract auditor BlockSec.Continue reading DeFi market overviewAnalytical data reveals that DeFi’s total value locked remained almost unchanged compared to the last week, registering a minor dip of $200 million to sit around $124.8 billion. Data from Cointelegraph Markets Pro and TradingView reveals that DeFi’s top 100 tokens by market capitalization registered a week filled with volatile price action, with many getting back in the green.The weekly performance of several tokens saw a bullish surge in double digits, barring a few tokens that remained in the red. In the top-100 DeFi list, 0x (ZRX) was the biggest gainer with a surge of 22.5% over the past week, followed by PancakeSwap (CAKE) with a 16.85% surge. Terra (LUNA) bulls also made a comeback with a 15% surge in the last week.Before you go!Another update on Axie Infinity’s stolen funds: Binance has frozen nearly $5.8 million of the stolen funds after the hacker group tried to move it using 86 accounts. Binance CEO Changpeng Zhao wrote earlier today:“The DPRK hacking group started to move their Axie Infinity stolen funds today. Part of it was made to Binance, spread across over 86 accounts. $5.8M has been recovered. We [have] done this many times for other projects in the past too.”Thanks for reading our summary of this week’s most impactful DeFi developments. Join us again next Friday for more stories, insights and education in this dynamically advancing space.

Čítaj viac