Data shows Bitcoin traders’ neutral view ahead of Friday’s $750M BTC options expiry

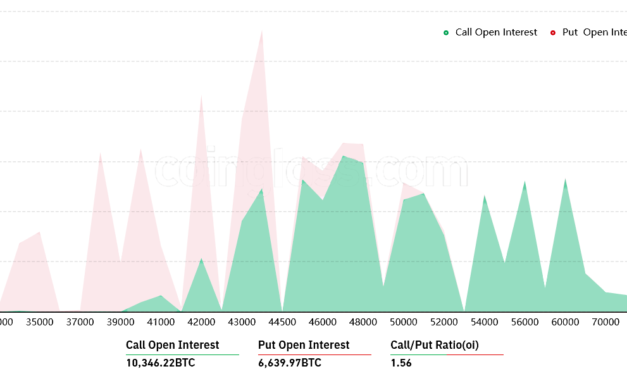

Bitcoin (BTC) has bounced 11% from the $39,650 low hit on Jan. 10 and, currently, the price is battling with the $44,000 level. There are multiple explanations for the recent weakness, but none of them seem sufficient enough to justify the 42% correction that took place since the Nov. 10 all-time high at $69,000.At the time (Nov. 12), negative remarks from the U.S. Securities and Exchange Commission (SEC) were issued at the rejection of VanEck’s physical Bitcoin exchange-traded fund (ETF). The regulatory body cited the inability to avoid market manipulation due to unregulated exchanges and heavy trading volume based on Tether’s (USDT) stablecoin.Then, on Dec. 17, the U.S. Financial Stability Oversight Council recommended that state and federal regulators review regulations and the tools that could be applied to digital assets. On Jan. 5, BTC price corrected again after the Federal Reserve’s December Federal Open Market Committee (FOMC) session, which confirmed plans to ease debt buyback and likely increase interest rates.Regarding derivatives markets, if Bitcoin price trades below $42,000 by the Jan. 14 expiry, bears will have a $75 million net profit on their BTC options.Bitcoin options aggregate open interest for Jan. 14. Source: CoinglassAt first sight, the $455 million call (buy) options are overshadowing the $295 million puts, but the 1.56 call-to-put ratio is deceptive because the 14% price drop over the last three weeks will likely wipe out most of the bullish bets.If Bitcoin’s price remains below $44,000 at 8:00 am UTC on Jan. 14, only $44 million worth of those call (buy) options will be available at the expiry. There is no value in the right to buy Bitcoin at $44,000 if BTC is trading below that price.Bears might bag a $75 million profit if BTC is below $42,000Here are the four most likely scenarios for the $750 million options expiry on Jan. 14. The imbalance favoring each side represents the theoretical profit. In practice, depending on the expiry price, the quantity of call (buy) and put (sell) contracts becoming active varies:Between $40,000 and $43,000: 480 calls vs. 2,220 puts. The net result is $75 million favoring the put (bear) options.Between $43,000 and $44,000: 1,390 calls vs. 1,130 puts. The net result is balanced between call and put options.Between $44,000 and $46,000: 1,760 calls vs. 660 puts. The net result is $50 million favoring the call (bull) options.Between $46,000 and $47,000: 1,220 calls vs. 520 puts. The net result is $125 million favoring the call (bull) options.This crude estimate considers put options being used in neutral-to-bearish bets and call options exclusively in bullish trades. However, this oversimplification disregards more complex investment strategies.For instance, a trader could have sold a put option, effectively gaining a positive exposure to Bitcoin above a specific price. But, unfortunately, there’s no easy way to estimate this effect.Related: Traders say Bitcoin run to $44K may be a relief bounce, citing a repeat of December’s ‘nuke’ Bulls need $46,000 for a decent winThe only way bulls can score a significant gain on the Jan. 14 expiry is by sustaining Bitcoin’s price above $46,000. However, if the current short-term negative sentiment prevails, bears could easily pressure the price down 4% from the current $43,800 and raise the profit by up to $75 million if Bitcoin price stays below $42,000.Currently, options markets seem balanced, giving bulls and bears equal odds for Friday’s expiry.The views and opinions expressed here are solely those of the author and do not necessarily reflect the views of Cointelegraph. Every investment and trading move involves risk. You should conduct your own research when making a decision.

Čítaj viac