EdgeX blames ‘external party’ for token crash as ZachXBT alleges insider manipulation

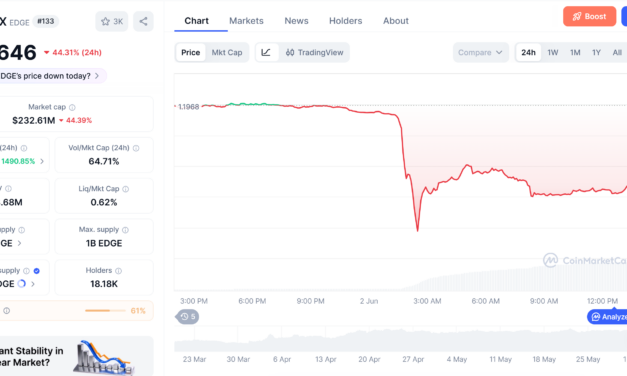

Decentralized exchange edgeX has attributed a more than 40% collapse in its EDGE token to ‘deliberate’ market manipulation by an unnamed external party, a claim that onchain investigator ZachXBT has dismissed.Data from CoinMarketCap shows edgeX (EDGE) plunged from roughly $1.20 to an intra-day low of $0.3663 on Tuesday, a drop of around 70%. The token is currently trading at $0.6474, down by around 45% over the past day.In a post on X, the edgeX team acknowledged the sudden collapse in its native token, telling its community it had “observed a sudden and irregular price movement” and was actively investigating.In response, ZachXBT claimed edgeX’s supply had been controlled by a small number of insiders operating with a low float, making the token inherently vulnerable to these types of events. He also demanded that the project publicly disclose the counterparties and market-maker agreements that contributed to the crash.Only 350 million EDGE tokens are currently in circulation out of a maximum supply of 1 billion, meaning more than two-thirds of the total supply has yet to hit the market. A low circulating float can make a token more vulnerable to sharp price moves, especially if liquidity is concentrated or large holders sell into thin order books.Related: Verus bridge exploiter returns $8.5M after bounty offerEdgeX says project not hackedIn a follow-up statement, edgeX said the platform had not been compromised in any way. “What we have identified so far suggests deliberate attempts by certain external party to manipulate the market price of EDGE,” the project wrote, calling it a market integrity issue.However, ZachXBT was unconvinced. “We investigated ourselves and did not find ourselves guilty even though we control nearly the entire supply,” he sarcastically wrote.Source: CoinMarketCapEdgeX is the 16th largest DEX in terms of trade volume over the past day, according to data from DefiLlama. The project has a total value locked (TVL) of $137 million.Related: Recovery hopes fade as Kelp DAO hacker launders nearly all $220M in stolen fundsDEX trading volume declinesDEX trading volume across all chains has also pulled back sharply from its peak levels.The broader pullback in DEX activity can make thinly traded tokens more vulnerable to sharp moves, though EDGE’s crash also involved project-specific questions over supply, market makers and insider control.After hitting a spike close to $45 billion in early 2025, aggregate decentralized exchange volume has trended lower and largely stabilized in the $5 billion to $20 billion daily range through the first half of 2026, with a secondary peak around $30 billion in October 2025 before fading again, according to data from DefiLlama.DEX trade volume. Source: DefiLlamaThe cooling activity reflects a broader retreat in onchain trading appetite following the frenzy of early 2025, leaving DEX markets thinner and more vulnerable to outsized price impacts.Magazine: The legal battle over who can claim DeFi’s stolen millions

Čítaj viac