Does Botanix’s failure prove Bitcoiners don’t care about DeFi?

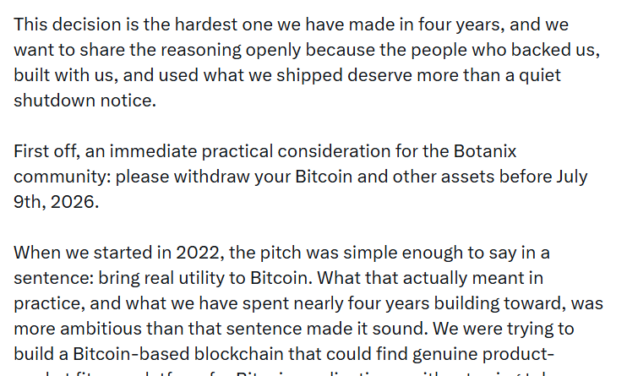

For the past two cycles, Bitcoin DeFi has lived more as a promise than a category.Programmable Bitcoin has remained a vision held by a certain breed of Bitcoin maxi who believes that the world’s largest cryptocurrency can become productive without losing its security or sound money qualities. Yet the closure of Bitcoin scaling platform Botanix earlier this month has called that vision into question.If a well-funded, technically ambitious Bitcoin layer-2 with live apps, integrations and competitive yields can’t attract enough usage to survive, does that mean Bitcoiners simply don’t care about decentralized finance?Bitcoin DeFi remains a niche proposition in 2026, despite years of being touted as the next big thing.DefiLlama’s dashboard shows just $4.12 billion of total value locked (TVL) across all of the Bitcoin DeFi protocols. That’s a rounding error next to Bitcoin’s $1.2 trillion market cap, and the hundreds of billions held via spot exchange-traded funds, corporate treasuries and custodial accounts.Andre Dragosch, head of research Europe at Bitwise, told Cointelegraph, “Bitcoin is winning decisively as a monetary asset and as pristine collateral, but the case for Bitcoin as a standalone DeFi execution layer was always structurally weaker than the narrative suggested.”Botanix closes after four yearsWhen Botanix announced it was winding down after nearly four years of work and a year of mainnet uptime, the team didn’t blame a hack or a regulatory shock; they blamed demand. Botanix described a chain that “worked” in every technical sense: 25 million transactions, 200,000 wallets, and tens of millions of dollars in bridged funds, yet it never generated the fee volume needed to cover its infrastructure costs. Users came for the yield, treated BTC as store-of-value collateral, and then largely stuck to passive, buy-and-hold strategies, rather than actively borrowing, trading, or moving funds often enough to generate meaningful fee volume. Related: Fireblocks to integrate Stacks for institutional-grade Bitcoin DeFi Like most BTCFi stacks today, Botanix still requires users to bridge their Bitcoin into a tokenized version on a separate Ethereum Virtual Machine (EVM)-based chain before they can access DeFi. That introduces additional bridge and smart contract assumptions that worry many Bitcoiners. Botanix’s shutdown notice. Source: BotanixEven so, Botanix co-founder Willem Schroé told Cointelegraph that he wouldn’t have changed the core design. Despite Botanix offering what he described as “the best rates in the industry” and a more Bitcoin-aligned security model than typical wrapped BTC bridges, wrapped BTC on Ethereum still out-competed Botanix.He attributed that to Ethereum’s “huge infrastructure network and Lindy effect,” as well as a mix of liquidity depth, user experience and regulatory comfort.What Botanix learned about Bitcoin DeFiThe team concluded that Bitcoin is still viewed as a reserve asset rather than something that has programmable utility. For most existing use cases like lending, leveraged exposure, or yield, a wrapped BTC position on a large, mature EVM ecosystem such as Ethereum is “genuinely sufficient” for most users. Rather than bridge into a Bitcoin-aligned EVM chain like Botanix, users preferred to stick with wBTC on venues where the liquidity, apps and integrations already exist.Related: Mercado Bitcoin expands LatAm RWA push with $20M in Rootstock private credit Botanix also pointed to onchain activity consolidating around venues like Hyperliquid, and major centralized exchanges and retail-facing fintechs that “own the user relationship,” leaving independent infrastructure “rowing upstream” against convenience and branding.Wilhelm said he hopes Botanix’s wind-down “will definitely be looked at by others,” and framed the process as a professionally managed experiment whose lessons other BTCFi builders should take seriously. Bitcoiners, DeFi and wrapped BTCWhile estimates vary, only a small fraction of Bitcoin’s supply is currently productive in DeFi, and most of that sits in wrapped BTC products on Ethereum and its L2s like Base and Arbitrum, as well as Polygon, Solana and BNB Smart Chain. A smaller percentage is on “Bitcoin L2” chains, with Bitcoin-aligned L2s and sidechains accounting for a modest share of that activity by value.Tokenized BTC products themselves represent just a sliver of the asset: A May 2026 analysis estimated that roughly $20 billion worth of BTC — less than 2% of the total Bitcoin supply — is circulating on EVM chains in wrapped form.Total Value Locked (TVL) in Bitcoin DeFi. Source: DeFiLlamaAn October 2025 GoMining survey of 730 Bitcoin holders found that 77% of respondents had never used a BTCFi platform, and only 3% integrated BTCFi into their overall Bitcoin strategy. Even allowing for sample bias (these respondents were plugged-in, survey-answering BTC holders), the numbers show that BTCFi platforms that keep users in Bitcoin-aligned stacks remain a niche activity rather than a mass behavior.Justin d’Anethan, head of research at crypto private markets advisory firm Arctic Digital, told Cointelegraph, “There is more liquidity and better yields on EVM or SVM [Solana Virtual Machine] native solutions than on BTC solutions, period.” When clients ask about “putting their Bitcoin to work,” the practical routes, he said, are still centralized desks, exchanges lending out BTC at 2% to 4%, basis trade structures “à la Ethena,” or institutional credit pools like Maple. Related: Bitcoin recovery meets DeFi tensions as Aave rift deepens: Finance RedefinedHe said the big obstacle for most Bitcoiners was the risk of bridging to a less secure Bitcoin L2. For “hardcore BTC maxis,” the default remains cold storage, HODLing and riding price appreciation, rather than trying to “eke out 2-3% with counterparty risk.”Native BTCFi as a structural mismatchDragosch said Botanix’s failure suggested that demand for standalone Bitcoin DeFi execution layers was much weaker than their backers expected.He argued that capital that “genuinely wants yield has migrated to wrapped BTC on mature, liquid venues rather than bridging into bespoke federations.” In this view, the problem isn’t just that Bitcoiners haven’t “discovered” native DeFi yet; it’s that the architecture and user base are misaligned. Bitcoin’s base layer is slow, conservative and firmly anchored in the store-of-value narrative.“Bitcoin as reserve collateral is the durable trade,” Dr. Dragosch said, “the next leg of adoption runs through institutions and balance sheets, not necessarily through onchain execution layers.”77% of respondents have never used a BTCFi platform. Source: GoMiningWho is still building BTCFi, and for whom?Diego Gutierrez Zaldivar, chief executive of RootstockLabs, a Bitcoin-secured, EVM-compatible sidechain, doesn’t buy the idea that there’s “no demand” for Bitcoin-backed lending, yield products or broader BTCFi services. He said the main constraint is trust: putting in place the operational, legal and risk management frameworks that institutions need. More than 40% of all Bitcoin DeFi activity now runs through Rootstock, he said, including real-world asset settlements and institutional vaults. Over the past year, he said, funds have started asking to deposit hundreds or even thousands of BTC at a time into Rootstock-based products; flows that were almost unheard of two or three years ago.Chains TVL. Source: DeFiLlamaOrkun Mahir Kılıç, co-founder of Chainway Labs, which is behind Citrea, a Bitcoin-anchored rollup combining the Bitcoin Virtual Machine (BVM) and zero-knowledge proofs, argued that cloning EVM DeFi primitives onto Bitcoin is a dead end, and said that Botanix’s experience is a verdict on that model, rather than BTCFi itself.Orkun Mahir Kılıç is co-founder of Chainway Labs, behind Citrea, a Bitcoin-anchored rollup that keeps user assets inside Bitcoin’s security perimeter and proves its state with zero-knowledge proofs. He argued that cloning EVM DeFi primitives onto Bitcoin is a dead end, and said that Botanix’s experience is a verdict on that model, rather than BTCFi itself.He told Cointelegraph that “more secure” doesn’t change most people’s behavior.“People don’t price counterparty risk until something breaks,” he said. ”Where it matters” is for institutions and large holders that need trust-minimized transactions with no custodian to fail.“For everyone else, the reason to be here isn’t the security guarantee in the abstract; it’s the applications that don’t exist elsewhere.”Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

Čítaj viac